Steem

Een gestimuleerd, blockchain gebaseerd sociaal media platform.

Maart 2016

Noten van de vertaler

Vertaald door @stino-san (https://steemit.com/steem/@stino-san/steem-whitepaper-dutch-part-1).

Abstract

Steem is een blockchain databank dat het vormen van gemeenschappen en sociale interactie ondersteund met cryptogeld beloningen. Steem combineert concepten uit sociale media met lessen uit het bouwen van cryptogeld en hun gemeenschappen. Een belangrijk onderdeel bij het inspireren van deelname in elke gemeenschap, valuta of vrije markteconomie is een eerlijk boekhoudkundig systeem dat de bijdrage van elke persoon consequent weerspiegelt. Steem is de eerste cryptovaluta dat probeert om op nauwkeurige en transparante wijze een onbegrensd aantal personen te belonen die subjectief bijdragen aan de gemeenschap.

Inhoudsopgave

- Introductie

- Manieren Om Bij Te Dragen

- Consensus Algorithm

- Eliminating Transaction Fees

- Performance and Scalability

- Allocation & Supply

- The Power of Steem

- No Micropayments, Tips Optional

- Value is in the Links

- Solving the Cryptocurrency Onboarding Problem

- Solving the Cryptocurrency Liquidation Problem

- Censorship

- Solving Organic Discovery via Search Engine Optimization

- Shifting Toward Blockchain-based Attribution

- Replacing Advertising with Blockchain-based Content Rewards

- Conclusion

- References

Introductie

Collectief, heeft gebruikers gegenereerde inhoud miljarden dollars waarde gecreëerd voor de aandeelhouders van sociale media bedrijven zoals Reddit, Facebook en Twitter. In 2014 veronderstelde Reddit dat het platform zou verbeteren indien het iedereen die bijdroeg tot reddit.com door het plaatsen van verhalen, toevoegen van opmerkingen en stemmen, zou belonen met een eerlijk aandeel in Reddit. Inc.1. Steem is gericht op het ondersteunen van sociale media en online gemeenschappen door veel van zijn waarde terug te keren aan mensen die waardevolle bijdragen maken door hen te belonen met cryptogeld, en door dit process een valuta te creëren die in staat is om een brede markt te bereiken, met begrip voor mensen die nog moeten deelnemen aan een cryptogeld economie.

Er zijn een aantal belangrijke principes gebruikt om het ontwerp van Steem te leiden. Het meest belangrijke uitgangspunt is dat, iedereen die bijdraagt aan een onderneming, pro-rata eigendom, betaling of schuld moet krijgen van de onderneming. Dit principe is hetzelfde principe dat van toepassing is bij alle startups wanneer deze aandelen toewijzen bij het oprichten of tijdens de daaropvolgende financiering rondes.

Het tweede principe is dat alle vormen van kapitaal even waardevol zijn. Dit betekent dat degenen die hun schaarse tijd en aandacht bijdragen door het produceren en selecteren van inhoud voor anderen net even waardevol zijn als degenen die hun schaars geld bijdragen. Dit is het zweet eigen vermogen principe2 en is een concept waar voorafgaande cryptovaluta’s vaak moeite mee hadden met het te verstrekken aan meer dan enkele tientallen individuen.

Het derde principe is dat de gemeenschap producten produceert om haar leden te dienen. Dit principe word geïllustreerd door credit unions, voedsel co-ops, en het delen van gezondheid plannen, welke hun leden dienen in plaats van het verkopen van producten en diensten aan mensen buiten de gemeenschap.

De Steem gemeenschap bied de volgende diensten aan haar leden:

- Een bron van geselecteerd nieuws en commentaar.

- Een middel om kwalitatieve antwoorden te krijgen op gepersonaliseerde vragen.

- Een stabiele cryptovaluta gekoppeld aan de Amerikaanse dollar.

- Gratis betalingen.

- Jobs die bovenstaande diensten verstrekken aan andere leden.

Steem’s doelbewuste herschikking van economische stimulans heeft het potentieel om eerlijker en meer inclusieve resultaten te produceren voor alle betrokkenen dan de sociale media en cryptogeld platformen die het zijn voorafgegaan. Dit document zal de huidige economische stimulans verkennen en demonstreren hoe Steem’s stimulans kan leiden tot betere resultaten voor de meeste deelnemers.

Bijdrage Herkennen

Steem is van de grond af aan ontworpen om de belangrijkste belemmeringen voor adoptie en het maken van geld van een sociaal media gebaseerde economie aan te pakken. Onze stelling is dat dezelfde technieken die gebruikt worden voor de groei van grote sociale media platformen gebruikt kunnen worden om een succesvolle cryptovaluta op te starten. Economische stimulans mogelijk gemaakt door cryptogeld kan de groei van een nieuw sociaal media platform drastisch vergemakkelijken. Wij geloven dat het de synergie is tussen cryptogeld en sociale media dat Steem een krachtig voordeel kan geven in de markt.

De uitdaging voor Steem is het afleiden van een algoritme voor het bijhouden van individuele bijdragen dat door de meeste leden van de gemeenschap word aanzien als een eerlijke overweging van de subjectieve waarde van elke bijdrage. In een perfecte wereld zouden leden van de gemeenschap samenwerken om elkaars bijdrage te beoordelen en een eerlijke compensatie af te leiden. In de echte wereld, moeten algoritmen ontworpen worden op een manier dat deze resistent zijn voor opzettelijke manipulatie voor winst. Elk wijdverspreid misbruik van het score systeem can leiden tot gemeenschapsleden die het geloof verliezen in de gepercipieerde eerlijkheid van het economisch systeem.

Bestaande platformen werken op een één gebruikers, één stem-principe. Dit creëert een omgeving waar rangorde kan worden gemanipuleerd door ‘sybil attacks’ en de dienstverleners pro actief misbruikers moeten identificeren en blokkeren. Mensen proberen al om de Reddit, Facebook en Twitter score algoritmes te manipuleren wanneer de enige beloning webverkeer of censuur is.

De fundamentele rekeneenheid op het Steem platform is STEEM, een cryptogeld token. Steem werkt op basis van één-STEEM, één-stem. Onder dit model hebben mensen die het meest hebben bijgedragen aan het platform, zoals gemeten door hun rekening balans, het meeste invloed op de manier waarop bijdragen worden gescoord. Bovendien laat Steem leden alleen toe om te stemmen met STEEM wanneer de betrokkene zich toewijd aan een meerjaren vestigingsschema. Onder dit model hebben leden een financiële drijfveer om te stemmen op een manier dat de lange termijn waarde van hun STEEM maximaliseert.

Steem is ontworpen rondom een relatief eenvoudig concept: Ieders zinvolle bijdrage aan de gemeenschap moet worden opgenomen voor de waarde die het toevoegt. Wanneer mensen worden erkend voor hun zinvolle bijdragen, blijven ze bijdragen zodat de gemeenschap groeit. Elke onbalans in het geven en nemen binnen de gemeenschap is onhoudbaar. Uiteindelijk word de gever moe van het ondersteunen van de nemer en zal deze zich los maken van de gemeenschap.

De uitdaging is het creëren van een systeem dat in staat is te identificeren welke bijdragen en hun relatieve waarde nodig zijn op een manier dat kan geschaald worden naar een oneindig aantal mensen.

Een bewezen systeem voor het evalueren en belonen van bijdragen is de vrije markt. De vrije markt kan beschouwd worden als één enkele gemeenschap waar iedereen handelt met elkaar en beloningen worden toegewezen door winst en verlies. Het markt systeem beloont degenen die zorgen voor waarde aan anderen en straft degenen die meer waarde verbruiken dan ze produceren. De vrije markt ondersteunt veel verschillende valuta’s en geld is gewoon een product dat iedereen gemakkelijk vind om uit te wisselen.

Omdat de vrije markt een bewezen systeem is, is het verleidelijk om te proberen een vrije markt systeem te creëren waar consumenten van inhoud, producenten van inhoud rechtstreeks betalen. Echter, rechtstreekse betaling is inefficiënt en niet haalbaar voor het creëren van inhoud en selectie. De waarde van de meeste inhoud is zo laag ten opzichte van de cognitieve, financiële en alternatieve kosten geassocieerd met het maken van een betaling die weinig lezers verkiezen te fooien. De overvloed aan gratis alternatieven betekent dat de tenuitvoerlegging van een ‘paywall’ de leden elders zal drijven. Er zijn verscheidene pogingen geweest per-artikel microbetalingen te implementeren van lezers naar gebruikers, maar geen daar van zijn wijdverspreid.

Steem is ontworpen om effectieve microbetalingen voor alle soorten bijdragen in staat te stellen door het veranderen van de economische vergelijking. Lezers hoeven niet langer meer te beslissen of zij wel of niet iemand willen betalen uit hun eigen zak, in plaats daarvan kunnen ze inhoud omhoog of omlaag stemmen en Steem zal hun stemmen gebruiken om individuele beloningen te bepalen. Dit betekent dat mensen een gebruikelijke en bekende interface krijgen en niet langer de cognitieve, financiële en alternatieve kosten dragen die geassocieerd worden met traditionele microbetaling en fooi platformen.

Stemmen inbreng van leden van de gemeenschap is van cruciaal belang voor Steem om nauwkeurige betalingen toe te wijzen aan medewerkers. Stemmen kan daarom worden gezien als een cruciale bijdrage en waardig voor beloningen op zichzelf. Sommige platformen, zoals Slashdot, gebruiken meta-moderatie 3 als een manier voor rangorde en het belonen van eerlijke moderators. Steem kiest er voor degenen te belonen die het meest bijdragen aan de totale promotie van een stuk inhoud en beloond de kiezers proportioneel aan de ultieme beloning betaald aan de maker van de inhoud.

Er zijn andere vormen van bijdrage die Steem herkent en beloont op basis van objectieve metriek. Onder deze zijn: transactie validatie, proof of work mining, liquiditeit beloningen en het aangeven van misdragende blok producenten.

Manieren Om Bij Te Dragen

In dit gedeelte worden de ideeën achter Steem en de beloningen voor mensen die zorgen voor zinvolle en meetbare bijdrage van de Steem gemeenschap beschreven.

Bijdragen In Kapitaal

Er zijn twee items dat een gemeenschap kan aanbieden voor het aantrekken van kapitaal: schuld en eigendom. Degenen die eigendom kopen genereren winst wanneer de gemeenschap groeit, maar verliezen wanneer de gemeenschap krimpt. Degenen die schuld kopen word een zekere mate van belang verzekerd maar kunnen niet deelnemen aan een winst gerealiseerd door de groei van de gemeenschap. Beide soorten bijdragen van kapitaal zijn waardevol voor de groei van de gemeenschap en de waarde van zijn munt. Daarnaast zijn er twee manieren hoe eigendom kan worden gehouden: liquiditeit en vestiging. Vestigingseigendom maakt een verbintenis op lange termijn en kan niet worden verkocht voor een minimale periode.

Het Steem netwerk noemt deze verschillende activaklassen Steem (STEEM), Steem Power (SP) en Steem Dollars (SMD).

Steem (STEEM)

Steem is de fundamentele rekeneenheid op de Steem blockchain. Alle andere tokens ontlenen hun waarde aan de waarde van STEEM. In het algemeen zou STEEM moeten worden gehouden voor korte perioden wanneer liquiditeit nodig is. Iemand die het Steem platform tracht toe te treden of te verlaten zal STEEM moeten kopen of verkopen. Zodra STEEM gekocht is zou het moeten omgezet worden in SP of SMD om het effect van verwatering op lange termijn te beperken.

STEEM word steeds groter in aanbod met 100% per jaar als gevolg van niet SMD stimulans. Iemand die STEEM heeft zonder het te converteren naar SP wordt verdund met ongeveer 0.19% per dag. Hoewel het percentage hoog kan lijken, voor transacties die minder dan 10 dagen duren, is het nog steeds goedkoper dan kredietkaart kosten. Bovendien is de dagelijkse token creatie onbelangrijk naast de dagelijkse volatiliteit.

Iemand die Bitcoin of een andere cryptovaluta koopt en verkoopt 10 dagen later kon gemakkelijk 3% of meer verliezen als gevolg van prijsschommelingen. Iemand die Bitcoin koopt en verkoopt op dezelfde dag zal meestal meer dan 0.4% betalen aan markt vergoedingen alleen. Met andere woorden de inflatie is in feite onbelangrijk tijdens de periode dat het typisch individu STEEM heeft.

De meerderheid van de inflatie is in feite een boekhoudkundig artefact in plaats van een echte herverdeling van rijkdom. 90% van de niet-SMD inflatie word terug verdeeld aan de bestaande houders van STEEM evenredig aan de STEEM waarde van hun SP balans, waardoor van de inflatie meer een "split" gemaakt word. Alleen ongeveer 10% van de niet-SMD inflatie herverdeelt eigendom in het netwerk.

Steem Power (SP)

Start-up bedrijven vereisen inzet over een lange termijn. Degenen die hun geld investeren in een startup wachten jaren alvorens ze hun aandelen kunnen verkopen en winsten kunnen realiseren. Zonder een inzet over een langer termijn zou een startup dat extra kapitaal zoekt door middel van het verkopen van extra aandelen moeten concurreren met bestaande aandeelhouders die wensen uit te treden. Vakkundige investeerders willen hun kapitaal bijdragen om het bedrijf te laten groeien, maar de groei kan niet gebeuren indien het nieuwe kapitaal word weggegeven aan degenen die wensen uit te treden.

Er is aanzienlijke waarde verbonden aan een lange termijninzet want het stelt gemeenschappen in staat lange termijn plannen te maken. Lange termijn inzet van aandeelhouders zorgt er ook voor dat ze stemmen voor lange termijn groei in plaats van korte termijn pumps.

In de cryptogeld wereld, springen speculanten van valuta naar valuta voornamelijk gebaseerd op welke valuta er verwacht word op korte termijn te groeien. Steem wil een gemeenschap bouwen dat grotendeels eigendom is en volledig gecontroleerd word door mensen met een lang termijn perspectief.

Omdat Steem lange termijn groei wil aanmoedigen is het gebonden om 9 STEEM toe te wijzen aan Steem Power (SP) aandeelhouders voor iedere 1 STEEM dat het creëert om de groei te financieren door middel van bijdrage stimulans. Na verloop van tijd drijft dit de verhouding tussen de totale STEEM waarde van Steem Power tot de totale STEEM verhoudingen naar 9:1. (Het lijkt er op dat de verhouding iets groter zal zijn dan 9:1 als gevolg van aanhoudend netto Powering Up van de nieuw gedrukte STEEM.) Dit betekent eveneens dat langdurige houders bijna volledig beschermd zijn tegen de verdunning gebruikt om de groei te financieren.

SP kan alleen terug naar STEEM worden omgezet in 2 jaar via 104 gelijke, wekelijkse betalingen. ‘1 SP’ kan gezien worden als een aandeel in een poel van STEEM. Het netwerk voegt automatisch, elke block, STEEM toe aan de poel. Op elk moment kunnen gebruikers hun STEEM omzetten naar SP aan dezelfde verhouding als STEEM tot totale SP in de vesting poel. Het omzetten van STEEM naar SP zorgt niet voor verdunning bij bestaande houders van SP. Net zoals, elke keer STEEM word omgezet naar SP word dit gedaan aan de huidige verhouding. Individuen worden gegarandeerd meer STEEM in de toekomst te hebben dan ze hadden wanneer ze voor het eerst STEEM omzetten naar SP.

SP tegoeden zijn niet overdraagbaar en niet deelbaar behalve via de automatische terugkerende wissel verzoeken. Dit betekent dat SP niet makkelijk kan gewisseld worden op cryptogeld wissel platformen.

SP is een vereiste voor het voor en tegen stemmen van inhoud. Dit betekent dat SP een toegangs token is die de houders ervan exclusieve bevoegdheden verleent binnen het Steem platform.

Het overbrengen van STEEM naar SP word aangeduid met ‘Power Up’ (bekrachtigen) terwijl het overbrengen van SP naar Steem word aangeduid met ‘Power Down’ (ontkrachten). Bijvoorbeeld, men kan over een periode van 2 jaar STEEM ontkrachten met ‘Power Down’. Maar men kan eveneens ogenblikkelijk STEEM bekrachtigen met ‘Power Up’.

Steem Dollars (SMD)

Stabiliteit is een belangrijke eigenschap van succesvolle, globale economieën. Zonder stabiliteit, zouden mensen over de hele wereld niet in staat zijn lage cognitieve kosten te hebben terwijl ze betrokken zijn bij handel en besparingen. Omdat stabiliteit een belangrijk kenmerk is van succesvolle economieën, werden Steem Dollars ontworpen om stabiliteit te brengen in de wereld van cryptogeld en bij gebruikers van het Steem netwerk.

Steem Dollars werden gemaakt door een mechanisme vergelijkbaar aan dat van converteerbare obligaties, welke vaak gebruikt worden om startups te financieren. In de startup wereld, zijn converteerbare obligaties instrumenten van korte termijn schuld die kunnen omgezet worden naar eigendom aan een tarief dat beslist word in de toekomst, meestal tijdens een volgende subsidieronde. Een blockchain gebaseerd token kan worden gezien als eigendom in de gemeenschap terwijl een converteerbare obligatie gezien kan worden als een schuld aangewezen in een andere grondstof of valuta. De voorwaarden van de converteerbare obligatie laten de houder toe het steun token om te zetten aan de eerlijke marktprijs en met een minimale opzegtermijn. Het creëren van token-converteerbare-dollars stelt blockchains in staat hun netwerk effect te laten groeien, terwijl het, het rendement van token houders maximaliseert.

Steem Dollars worden aangeduid met het symbool SMD, een acroniem voor Steem Dollars. Het creëren van SMD vereist een combinatie van betrouwbare prijs feed, regels voor het voorkomen van misbruik en liquiditeit. Het verstrekken van een betrouwbare prijs feed bestaat uit drie factoren: de impact van een onjuiste feed minimaliseren, de kost van een onjuiste feed maximaliseren, en het belang van timing minimaliseren.

Fraude Feeds Minimaliseren

SP houders kiezen individuen om prijs feeds te publiceren. Deze verkozen individuen worden vermoedelijk vertrouwd door degenen met gevestigde belangen in de kwaliteit van de feed. Door degenen die verkozen zijn te betalen, creëert Steem markt concurrentie om het recht te verdienen om feeds te produceren. Hoe meer de producenten van feeds betaald worden hoe meer ze te verliezen hebben door het publiceren van valse informatie.

Gegeven een reeks vertrouwde en verkozen feed producenten, kan de werkelijke prijs gebruikt voor het omzetten afgeleid worden als het gemiddelde van de feeds. Op deze manier is het zo dat als een minderheid van individuele feed producenten uitschieters produceert, deze een minimale impact hebben op het werkelijke gemiddelde, terwijl het vermogen om hun reputatie te beïnvloeden behouden word.

Zelfs wanneer alle feed producenten eerlijk zijn, is het onmogelijk voor de meerderheid van feed producenten om beïnvloed te worden door gebeurtenissen buiten hun controle. Het Steem netwerk is ontworpen om de korte termijn corruptie van de gemiddelde prijs feed te tolereren, terwijl de gemeenschap actief werkt om de kwestie te corrigeren. Een voorbeeld van een probleem dat enige tijd kan duren om te corrigeren is korte termijn marktmanipulatie. Marktmanipulatie is moeilijk en duur om te onderhouden voor langere perioden. Een ander voorbeeld is het falen van een gecentraliseerd wisselplatform of de corruptie van de data gepubliceerd door het wisselplatform.

Steem elimineert korte termijn prijsschommelingen door het gebruik van de gemiddelde prijs over een periode van één week. De gemiddelde gepubliceerde feed word gesampled elk uur op het uur.

Zolang de prijs feed corruptie duurt voor minder dan de helft van het bewegend gemiddelde tijdsverloop zal het een minimale invloed hebben op de conversie prijs. In het geval dat de feed toch corrumpeert, zullen netwerk participanten de kans krijgen producenten van corrupte feed weg te stemmen voor de corrupte feed in staat is de werkelijke conversie prijs te beïnvloeden. Misschien van nog groter belang is dat het feed producers een kans geeft om problemen te detecteren en corrigeren nog voor hun feed de prijs begint te beïnvloeden.

Met een tijdsduur van één week, hebben gemeenschapsleden drie en een halve dag om te reageren op eventuele, onvoorziene problemen.

Timing Aanvallen Matigen

Marktdeelnemers hebben sneller toegang tot informatie dan de blockchain’s één-week bewegende, gemiddelde conversie prijs kan reageren. Deze informatie kan gebruikt worden in het voordeel van handelaren op kosten van de gemeenschap. Als er een plotselinge stijging plaatsvind in de waarde van STEEM zouden handelaren de omzetting van hun SMD kunnen aanvragen aan de oude, lagere prijs, en vervolgens de STEEM verkopen die ze ontvangen aan de nieuwe, hogere prijs met minimaal risico.

Steem creëert gelijke kansen door te eisen dat alle conversie verzoeken worden vertraagd voor één week. Dit betekent dat noch de handelaren, noch de blockchain enig informatie voordeel heeft betreffende de prijs op het moment dat de conversie word uitgevoerd.

Misbruik Van Conversies Minimaliseren

Wanneer mensen vrij zouden kunnen converteren in beide richtingen zouden handelaren kunnen profiteren van de blockchains conversiepercentages door te handelen in grote volumes zonder het veranderen van de prijs. Handelaren die een enorme aanloop zien in prijs zouden converteren naar SMD tegen de hoge prijs (wanneer het risico hoogst is) en vervolgens terug converteren na de correctie. Het Steem protocol beschermt de gemeenschap van dit soort misbruik door mensen alleen toe te laten van SMD naar STEEM te converteren en niet andersom.

De blockchain bepaalt hoe en wanneer SMD moet gemaakt worden en wie dit moet krijgen. Dit houd de snelheid van SMD creatie stabiel en verwijderd de meeste wegen naar misbruik.

Liquidity

Just because SMD can be converted to a dollars worth of STEEM at a fair price in a reasonable amount of time doesn't mean it will be viewed as a reliable dollar replacement. These assets require liquidity in a market that enables instantaneous conversion between STEEM and SMD. The measures a blockchain is forced to take to prevent abuse end up lowering the quality of the convertible dollars. To compensate for this loss of quality the blockchain can offer a fixed cost reward to liquidity providers. Whereas the potential losses from manipulation and abuse are unbounded, the cost of encouraging liquidity can be fixed.

A liquidity provider buys and sells SMD and STEEM. They take on the majority of the short-term price risk and long-term feed risk giving the remaining market participants a high quality, extremely liquid market within which to trade.

Steem has an on-blockchain market between SMD and STEEM. Users can earn rewards by providing liquidity to both sides of this market. The blockchain uses a simple algorithm to rank each user's liquidity provision and consumption.

A user is considered a liquidity provider if they leave an open order on the books for at least 1 minute and the order is eventually filled. If the order is canceled before being filled then the user is not credited with providing liquidity.

Users must provide liquidity on both sides of the book to qualify for rewards and they must provide liquidity consistently over time. The scoring algorithm is:

LiquidityPoints = NetBidVolume x NetAskVolume

Every hour the account with the most LiquidityPoints receives 1200 STEEM and then has its LiquidityPoints reset to 0. An account that goes a week without earning any LiquidityPoints also has its points reset to 0. This means that whether you provide a large amount of liquidity or a small amount over a long period of time everyone gets a proportional amount of the rewards. If either NetBidVolume or NetAskVolume is negative, then LiquidityPoints is considered to be 0.

Sustainable Debt to Ownership Ratios

If a token is viewed as ownership in the whole supply of tokens, then a token-convertible-dollar can be viewed as debt. If the debt to ownership ratio gets too high the entire currency can become unstable. Debt conversions can dramatically increase the token supply, which in turn is sold on the market suppressing the price. Subsequent conversions require the issuance of even more tokens. Left unchecked the system can collapse leaving worthless ownership backing a mountain of debt. The higher the debt to ownership ratio becomes the less willing new investors are to bring capital to the table.

For every SMD Steem creates, $19.00 of STEEM is also created and converted to SP. This means that the highest possible debt-to-ownership in a stable market is 1:19 or about 5%. If Steem falls in value by 50% then the ratio could increase to 10%. An 88% fall in value of STEEM could cause the debt-to-ownership ratio to reach 40%. Assuming the value of STEEM eventually stabilizes, the debt-to-ownership ratio will naturally move back toward 5%.

The idea behind having a conservative 5% debt to ownership ratio is that even if all debt were converted and sold there should be ample buyers and the effective dilution of the token holders remains relatively small.

A rapid change in the value of STEEM can dramatically change the debt-to-ownership ratio. The percentage floors used to compute STEEM creation are based on the supply including the STEEM value of all outstanding SMD and SP (as determined by the current rate / feed).

Interest

SMD pays holders interest. The interest rate is set by the same people who publish the price feed so that it can adapt to changing market conditions. All debt carries risk to the lender. Someone who holds SMD without redeeming it is effectively lending the community the value of a dollar. They are trusting that at some point in the future someone will be willing to buy the SMD from them for a dollar or that there will be speculators and investors willing to buy the STEEM they convert it into.

STEEM and SP holders gain leverage when members of the community are willing to hold SMD. This leverage amplifies the gains from growth while also contributing to growth. STEEM holders do suffer from increased dilution if the price falls. Cryptocurrency projects have shown that the gains from increasing the user base willing to trust the network with capital ultimately add more value to the network than any dilution that may occur during a downturn.

Setting Price Feeds

Astute readers will recognize that an interest bearing asset of limited supply may trade higher or lower than the underlying asset depending upon other opportunities to earn interest on the same asset. With a high interest rate paid on an asset pegged to the US dollar many people will bid up the limited supply of Steem Dollars until they are no longer valued at $1. In economics there is a principle known as the Impossible Trinity4 which states that it is impossible to have all three of the following at the same time:

- A stable exchange rate

- Free capital movement

- An independent monetary policy

If Steem feed producers aim to have an independent monetary policy allowing it to create and destroy Steem Dollars while simultaneously having full control over the interest rate then they will encounter problems. The Impossible Trinity says that Steem Dollars either need to restrict capital movement, have an unstable exchange rate with the dollar, or have limited control over the interest rate.

The primary concern of Steem feed producers is to maintain a stable one-to-one conversion between SMD and the U.S. Dollar (USD). Any time SMD is consistently trading above $1.00 USD interest payments must be stopped. In a market where 0% interest on debt still demands a premium, it is safe to say the market is willing to extend more credit than the debt the community is willing to take on. If this happens a SMD will be valued at more than $1.00 and there is little the community can do without charging negative interest rates.

If the debt-to-ownership ratio is under 10% and SMD is trading for less than $1.00 then the interest rate should be increased. This will encourage more people to hold their SMD and support the price.

If SMD trades for less than $1.00 USD and the debt-to-ownership ratio is over 10% then the feeds should be adjusted upward give more STEEM per SMD. This will increase demand for SMD while also reducing the debt-to-ownership ratio and returning SMD to parity with USD.

Assuming the value of STEEM is growing faster than Steem is creating new SMD, the debt-to-ownership ratio should remain under the target ratio and the interest offered benefits everyone. If the value of the network is at or falling, then any interest offered will only make the debt-to-ownership ratio worse.

In effect, feed producers are entrusted with the responsibility of setting monetary policy for the purpose of maintaining a stable peg to the USD. Abuse of this power can harm the value of STEEM so SP holders are wise to vote for witnesses that can be counted on to adjust the price feed and interest rates according to the rules outlined above.

If the debt-to-ownership ratio gets dangerously high and market participants choose to avoid conversion requests, then the feed should be adjusted to increase the rate at which STEEM paid for converting SMD.

Changes to the interest rate policy and/or any premiums/discounts on the STEEM/SMD conversion rate should be a slow and measured response to long-term average deviations rather than attempting to respond to short-term market conditions. The blockchain is paying liquidity providers for their service in absorbing short-term demands.

It is our belief that these rules will give market participants confidence that they are unlikely lose money by holding SMD purchased at a price of $1.00. We fully expect there to be a narrow trading range between $0.99 and $1.01 for SMD under most market conditions.

Subjective Contributions

Subjective Proof of Work presents an alternative approach to distributing a currency that improves upon fully objective Proof of Work systems such as mining. The applications of a currency implementing subjective proof of work are far wider than any objective proof of work system because they can be applied to build a community around any concept that has a sufficiently defined purpose. When individuals join a community they buy into a particular set of beliefs and can vote to reinforce the community values or purpose.

In effect, the criteria by which work is evaluated is completely subjective and its definition lives outside the source code itself. One community may wish to reward artists, another poets, and another comedians. Other communities may choose to reward charitable causes or help advance political agendas.

The value each currency achieves depends upon the demand for influence within a particular community and how large the market believes each community can get. Unlike prior systems, subjective proof of work enables a community to collectively fund the development of whatever it finds valuable and enables the monetization of previously non monetizable time.

Distributing Currency

There are two ways people can get involved with a crypto-currency community: they can buy in, or they can work in. In both cases users are adding value to the currency, however, the vast majority of people have more free time than they do spare cash. Imagine the goal of bootstrapping a currency in a poor community with no actual cash but plenty of time. If people can earn money by working for one another then they will bootstrap value through mutual exchange facilitated by a fair accounting/currency system.

Distributing a currency to as many people as possible in a manner that is generally perceived as fair is a challenging task. The tasks that can be entirely evaluated by an objective computer algorithm are limited in nature and generally speaking have limited positive external benefits. In the case of Bitcoin-style mining, it can result in the production of specialized hardware and cause people to invest time developing more efficient algorithms. It may even help find prime numbers, but none of these things provide meaningful value to society or the currency holding community at large. More importantly, economies of scale and market forces will end up excluding everyone but experts from participating in this kind of distribution. Ultimately, computation-based mining is just another way of buying in because it requires money to pay the electric bill or the development of hardware necessary to do the work.

In order to give everyone an equal opportunity to get involved and earn the currency people must be given an opportunity to work. The challenge is how to judge the relative quality and quantity of work that individuals provide and to do so in a way that efficiently allocates rewards to millions of users. This requires the introduction of a scalable voting process. In particular it requires that authority to allocate funds must be as distributed and decentralized as possible.

The first step in rewarding millions of users is to commit to distributing a fixed amount of currency regardless of how much work is actually done or how users vote. This changes the question from being "Should we pay?" to "Whom should we pay?" and signals to the market that money is being distributed and is being auctioned off to whoever "bids" the most work. This is similar to Bitcoin committing to award 50 BTC to whoever finds the most difficult hashes. Like Bitcoin, all work must be done prior-to payout and nothing should be paid speculatively on the promise to do work in the future.

The next step is to reward everyone who does anything even remotely positive with something. This is accomplished by ranking all work done and distributing proportionally to its value. The more competitive the market becomes, the more difficult (higher quality or quantity) it becomes to earn the same payout.

Voting on Distribution of Currency

Assume there is a fixed amount of money to distribute, and that those who have a long-term vested interest in the future value and utility of the currency are the ones who must decide how to allocate it. Every vesting user casts their votes on who did the best work and at the end of the day the available money for that day is divided proportional to the votes such that everyone with even one net positive vote gets something.

The naive voting process creates a Prisoner's Dilemma whereby each individual voter has incentive to vote for themselves at the expense of the larger community goal. If every voter defects by voting for themselves then no currency will end up distributed and the currency as a whole will fail to gain network effect. On the other hand, if only one voter defects then that voter would win undeserved profits while having minimal effect on the overall value of the currency.

In order to realign incentives and discourage individuals from simply voting for themselves, money must be distributed in a nonlinear manner. For example a quadratic function in votes, i.e., someone with twice the votes of someone else should receive four times the payout and someone with three times the votes should receive nine times the payout. In other words, the reward is proportional to \(votes^{2}\) rather than votes. This mirrors the value of network effect which grows with \(n^{2}\) the number of participants, according to Metcalfe's Law5.

Assuming all users have equal stake, someone who only receives their own vote will receive much less than someone who receives votes from 100 different users. This encourages users to cooperate to vote for the same things to maximize the payout. This system also creates financial incentive to collude where everyone votes on one thing and then divides the reward equally among themselves.

Voting Collusion

While cooperation to distribute funds to the best work is the desired goal, collusion that undermines this objective should be minimized. There are two kinds of collusion, the most straightforward is when one user simply buys a larger stake than others, and the other involves coordinating a large number of smaller stakeholders to work together. Larger stakeholders can have the voting influence of 100 or even 1000 smaller stakeholders which means they have even greater incentive to defect by voting for themselves than they had under a linear distribution.

Regardless of how much money any one individual has, there are always many other individuals with similar wealth. Even the wealthiest individual rarely has much more than the next couple wealthiest combined. Furthermore, those who have a large investment in a community also have the most to lose by attempting to game the voting system for themselves. It would be like the CEO of a company deciding to stop paying salaries so he could pocket all of the profits. Everyone would leave to work for other companies and the company would become worthless, leaving the CEO bankrupt rather than wealthy.

Fortunately, any work that is getting a large concentration of votes is also gaining the most scrutiny (publicity). Through the addition of negative-voting it is possible for many smaller stakeholders to nullify the voting power of collusive groups or defecting large stakeholders. Furthermore, large-stakeholders have more to lose if the currency falls in value due to abuse than they might gain by voting for themselves. In fact, honest large stakeholders are likely to be more effective by policing abuse and using negative voting than they would be by voting for smaller contributions.

The use of negative-voting to keep people from abusing the system leverages the crab mentality that many people have when it is perceived that one individual is profiting at the expense of everyone else. While crab mentality normally refers to short-sighted people keeping good people down, it is also what allows good people to keep bad people down. The only "problem" with crab mentality is when people wrongly believe someone is profiting at everyone else's expense.

The Story of the Crab Bucket6

A man was walking along the beach and saw another man fishing in the surf with a bait bucket beside him. As he drew closer, he saw that the bait bucket had no lid and had live crabs inside.

"Why don't you cover your bait bucket so the crabs won't escape?", he said.

"You don't understand.", the man replied, "If there is one crab in the bucket it would surely crawl out very quickly. However, when there are many crabs in the bucket, if one tries to crawl up the side, the others grab hold of it and pull it back down so that it will share the same fate as the rest of them."

So it is with people. If one tries to do something different, get better grades, improve herself, escape her environment, or dream big dreams, other people will try to drag her back down to share their fate.

Eliminating "abuse" is not possible and shouldn't be the goal. Even those who are attempting to "abuse" the system are still doing work. Any compensation they get for their successful attempts at abuse or collusion is at least as valuable for the purpose of distributing the currency as the make-work system employed by traditional Bitcoin mining or the collusive mining done via mining pools. All that is necessary is to ensure that abuse isn't so rampant that it undermines the incentive to do real work in support of the community and its currency.

The goal of building a community currency is to get more "crabs in the bucket". Going to extreme measures to eliminate all abuse is like attempting to put a lid on the bucket to prevent a few crabs from escaping and comes at the expense of making it harder to add new crabs to the bucket. It is sufficient to make the walls slippery and give the other crabs suf cient power to prevent others from escaping.

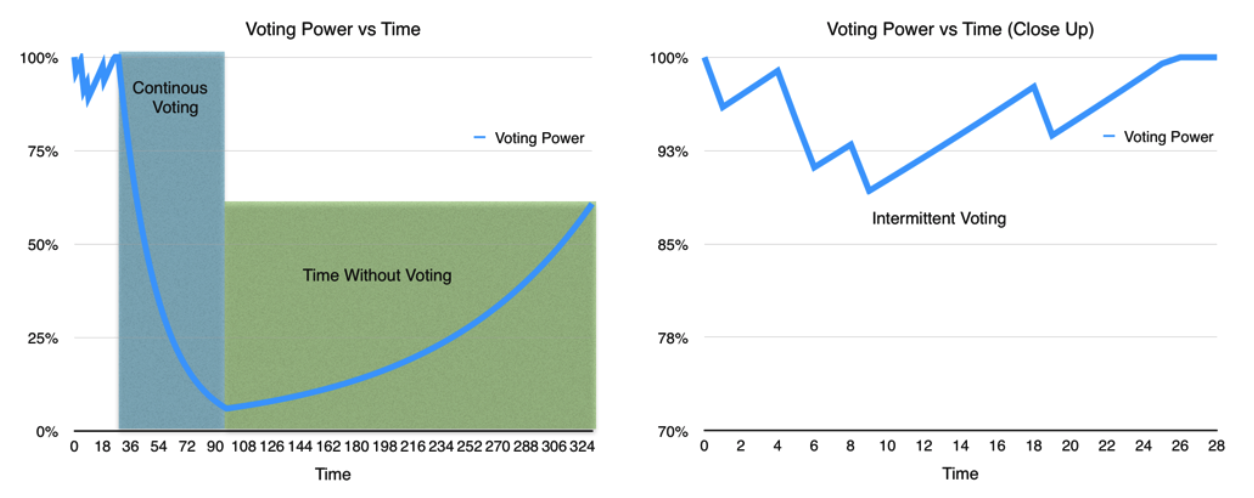

Rate Limited Voting

A major part of minimizing abuse is the rate-limiting of voting. Individual users can only read and evaluate so many work items per day. Any attempt to vote more frequently than this is a sign of automation and potential abuse. Through rate limiting, stakeholders who vote more frequently have each vote count for less than stakeholders who vote less frequently. Attempts to divide tokens among multiple accounts also divides influence and therefore does not result in a net increase in influence nor bypass the rate-limit imposed on voting.

The charts above shows how a user's voting power decreases every time they vote and then regenerates as time passes without voting. These charts use nominal time unit and could be made to scale to any targeted voting rate. Note that voting power rapidly drops off during periods of continuous voting, and then slowly recovers.

Voting power is multiplied by a user's vesting tokens to determine how much share in the reward pool should be allocated to a given work item.

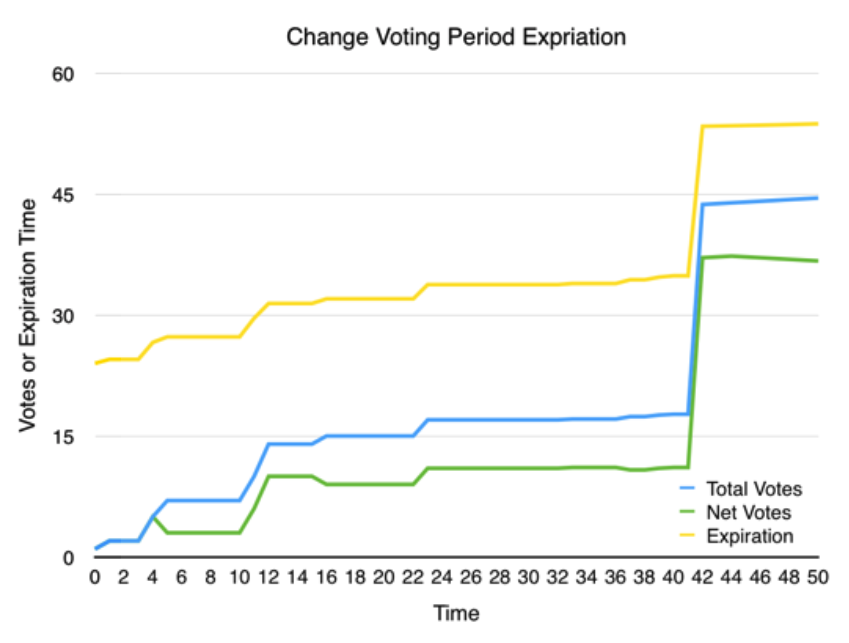

Delayed Payouts

To further prevent abuse, all payouts are delayed a stake-weighted average of 24 hours from the time each vote was cast. This ensures that large stakeholders cannot snipe payouts by voting at the last second before other voters (aka crabs) have a chance to negate the potential abuse. Once a payout is made to the user all votes are reset to 0. If votes come in after the payout then the process begins again.

This chart shows how the voting period expiration changes in response to new positive and negative votes being applied. New votes extend the payout period in proportion to how large they are relative to all votes that have gone before. Around time 40 a large number of new votes were added which extended the voting period by 12 hours, subsequent smaller votes had far less impact on the voting period.

Payout Distribution

One of the primary goals of Steem's reward system is to produce the best discussions on the internet. Each and every year 10% of the market capitalization of Steem is distributed to users submitting, voting on, and discussing content. At the size of Bitcoin this could be as much as $1.75 million dollars per day being given to top contributors.

The actual distribution will depend upon the voting patterns of users, but we suspect that the vast majority of the rewards will be distributed to the most popular content. Steem weighs payouts proportional to \(n^{2}\) the amount of Steem Power voting for a post. In other words, post x would receive a payout proportional to:

\(votes[x]^{2} / sum(votes[0...n]^{2})\)

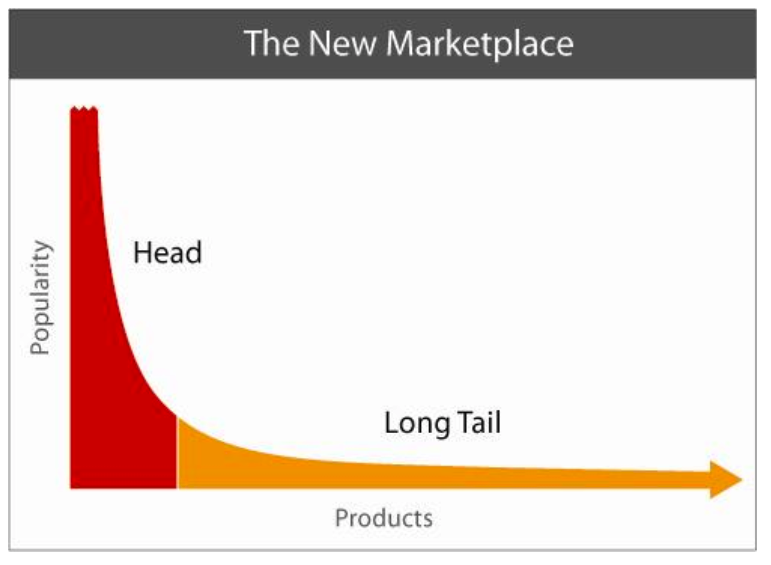

Zipf's Law7 is one of those empirical rules that characterize a surprising range of real-world phenomena remarkably well. It says that if we order some large collection by size or popularity, the second element in the collection will be about half the measure of the first one, the third one will be about one-third the measure of the first one, and so on. In general, the \(k^{th}\)-ranked item will measure about 1/k of the first one.

Taking popularity as a rough measure of value, then the value of each individual item is given by Zipf's Law. That is, if we have a million items, then the most popular 100 will contribute a third of the total value, the next 10,000 another third, and the remaining 989,900 the final third. The value of the collection of n items is proportional to log(n).

The impact of this voting and payout distribution is to offer large bounties for good content while still rewarding smaller players for their long-tail contribution.

The economic effect of this is similar to a lottery where people over-estimate their probability of getting votes and thus do more work than the expected value of their reward and thereby maximize the total amount of work performed in service of the community. The fact that everyone "wins something" plays on the same psychology that casinos use to keep people gambling. In other words, small rewards help reinforce the idea that it is possible to earn bigger rewards.

Rewarding Parent Posts

Good discussion requires back and forth posting. When you reply to someone else, they get 50% of any payout you receive in that thread. This rule applies up to 6 levels deep. Starting a big discussion greatly rewards the parent poster.

Failure to properly nest your posts in the discussion is a good way to get down voted.

This incentive structure motivates people to contribute in a way that motivates others to get involved. It encourages people to ask good questions so that others can provide valuable answers.

Payouts

When a post receives a payout it takes the form of 50% SMD and 50% SP. The Steem Power give the user increased voting and transaction power while the SMD gives the user an immediate benefit in a stable currency. As we've already discussed at length, both SP and SMD are designed to encourage long-term holding rather than short-term selling.

Consensus Algorithm

Consensus is the process by which a community comes to a universally recognized, unambiguous agreement on piece of information. There are many algorithms society has developed for reaching consensus about who owns what. Every government on earth is a primitive consensus algorithm whereby the population agrees to abide by a certain set of rules enshrined in a constitution. Governments establish courts, judges, and juries to interpret the subjective facts and render a final decision. Most of the time people abide by the decision even if it was wrong.

The algorithms used by cryptocurrencies provide a better way to reach consensus. Cryptographically signed testimony from individuals is recorded in a public ledger that establishes the absolute global order of events. A deterministic computer algorithm can then process this ledger to derive a universally accepted conclusion. So long as the members of a community agree on the processing algorithm, the result of the algorithm is authoritative.

The primary consideration is determining what testimony is allowed to enter the public record. Systems should be designed to minimize the potential for censorship. Censorship on the public ledger is similar to preventing someone from voting in an election. In both cases an individual is prevented from impacting the global consensus.

Consensus in Steem

Conceptually, the consensus algorithm adopted by Steem is similar to the consensus algorithm adopted by companies throughout the world. People with a vested interest in the future value of Steem vote to select individuals responsible for including testimony in the public record. Voting is weighted proportional to each individual's vested interest.

In the world of cryptocurrencies, the public record is commonly referred to as a blockchain. A block is a group of signed transactions.

With Steem, block production is done in rounds. Each round 21 witnesses are selected to create and sign blocks of transactions. Nineteen (19) of these witnesses are selected by approval voting, one is selected by a computational proof-of-work, and one is timeshared by every witness that didn't make it into the top 19 proportional to their total votes. The 21 active witnesses are shuffled every round to prevent any one witness from constantly ignoring blocks produced by the same witness placed before.

This process is designed to provide the best reliability while ensuring that everyone has the potential to participate in block production regardless of whether they are popular enough to get voted to the top. People have three options to overcome censorship by the top 19 elected witnesses: patiently wait in line with everyone else not in the top 19, purchase enough computational power to solve a proof of work faster than others, or purchase more SP to improve voting power. Generally speaking, applying censorship is a good way for elected witnesses to lose their job and therefore, it is unlikely to be a real problem on the Steem network.

Because the active witnesses are known in advance, Steem is able to schedule witnesses to produce blocks every 3 seconds. Witnesses synchronize their block production via the NTP protocol. A variation of this algorithm has been in use by the BitShares network for over a year where it has been proven to be reliable.

Mining in Steem

Traditional proof of work blockchains combine block production with the solving of a proof of work. Because the process of solving a proof of work takes an unpredictable amount of time, the result is unpredictable block production times. Steem aims to have consistent and reliable block production every 3 seconds with almost no potential for forks.

To achieve this Steem separates block production from solving of proof of work. When a miner solves a proof of work for Steem, they broadcast a transaction containing the work. The next scheduled witness includes the transaction into the blockchain. When the transaction is included the miner is added to the queue of miners scheduled to produce blocks. Each round one miner is popped from the queue and included in the active set of witnesses. The miner gets paid when they produce a block at the time they are scheduled.

The difficulty of the proof of work doubles every time the queue length grows by 4. Because one miner is popped from the queue every round, and each round takes 21 * 3 = 63 seconds, the difficulty automatically halves if no proof of work is found in no more than 21 * 3 * 4 = 252 seconds.

Mining Rewards require Steem Power

After the first month, Steem miners are paid in Steem Power (SP). SP is liquidated through the two-year process of "powering down". This means that miners must wait for a long time, likely many months, before sufficient mining rewards have been powered down to allow them to recover the cost of electricity and computational resources. The powering down process discourages creation of mining pools because the pool operator would have to spread payouts over years.

The effect of paying mining rewards in SP is to prevent miners from using today's price to determine the pro tability of mining. Few people will agree on what the future price will be. This means mining difficulty will be driven by those who place the highest estimate on future value. Miners without a long-term interest in the platform will be discouraged from competing. Ultimately this means that the proceeds of mining are less likely to be dumped on the market because they will accrue to long-term believers in the platform.

Mining Algorithm

The mining algorithm adopted by Steem requires the miner to have access to the private key of the account that will receive the rewards. This requirement has several important consequences. First it encourages optimization of elliptic curve signature verification algorithms needed by Steem. Second it makes it challenging to set up mining pools because the pool operator would have to share control over the reward with all of the "anonymous" miners. Third, it makes it difficult to use botnets because the botnet operator would have to distribute their private key to all compromised machines.

The following pseudocode describes how the proof-of-work hash value is calculated:

Let H = Head Block ID

Let H2 = SHA256(H + NONCE)

Let PRI = Producer Private Key

Let PUB = Producer Public Key

Let S = SIGN(PRI, SHA256(H))

Let K = RECOVER_PUBLIC_KEY(H2, S)

Let POW = SHA256(K)

Botnet Resistant

Many proof of work coins end up being mined by botnets. A botnet is a collection of thousands or millions of machines that have been compromised by hackers. These hackers steal the computational and electrical resources of compromised machines to mine cryptocurrency tokens.

Steem has many properties that prevent these computational thieves from profiting. Botnet operators are profit seeking enterprises and typically sell their stolen resources to the highest bidder. This means that those who utilize a botnet pay for the computational power in the same way that someone who uses Amazon EC2 does. The vesting requirement of Steem means that the capital spent on buying the resources of the botnet will be tied up for a long period of time during which the operator is exposed to price volatility.

Another way that botnet operators are prevented from profiting is the requirement to distribute the private key to all compromised machines. If even one compromised computer is discovered, the operator could lose their coins.

The last mitigation is the dependency on latency. Most botnets are comprised of computers with poor internet connections, these slow Internet connections will dramatically reduce the effectiveness of the computational resource.

It should be more profitable and less risky for botnet operators to use their resources for other activities than mining STEEM.

Mining Pool Resistant

Miners have a total of 3 seconds to receive a block, solve the proof of work, and get the transaction to the next block producer. Much of this time will consist of network latency which means that it is critical for miners to be well connected to the network to make the most effective use of their computational resources.

Because of the constantly changing head block and network latency, forwarding a template for mining a specific block to participants of a mining pool adds additional network latency and reduces efficiency of pooled mining significantly.

Eliminating Transaction Fees

Steem goes to great lengths to reward people for contributing to the network. It would be counterproductive to turn around and charge people every time they attempt to interact with the community.

Blockchain technology currently depends upon transaction fees to prevent spam. These fees suffer all of the known problems with microtransactions and prevent blockchains from being used for low-value transactions. Truly decentralized applications must offer users the appearance of free transactions if they wish to compete with their centralized alternatives. This paper outlines the approach used by Steem to eliminate the need for fees and thereby enable a wide range of previously untenable decentralized applications.

The Problem With Fees

Blockchains are decentralized networks where all transactions are broadcast to all peers. Every so often a block is produced that includes some or all of the pending transactions. All blockchains must find a solution to prevent malicious users from consuming all of the available network capacity with worthless transactions. These worthless transactions can prevent other valuable transactions from being processed and ultimately destroy the network.

The solution adopted by most blockchains thus far is to charge a minimum transaction fee. A fee worth just a few cents is enough to make attacking the network expensive and unprofitable. While this approach solves the spam problem, it introduces new problems. Imagine solving the email spam problem by introducing a small fee on every email; people wouldn't use email.

Micropayments Don't Work

The fundamental problem with charging transaction fees is that micropayments don't work, especially for low-value user actions. When a fee is charged on every transaction, it limits the types of transactions that a decentralized network can process. Regardless of how rational the argument for the necessity of fees, users still hate the experience of being nickeled and dimed for everything that they do.

Imagine if the websites we use every day charged us a fee every time we modify our accounts by changing the password. Users expect certain things to be free. Requiring users to make a decision on whether or not an action is worth a small fee creates anxiety that causes users to leave.

A transaction can't be worth so much as to require a decision but worth so little that that decision is automatic. There is a certain amount of anxiety involved in any decision to buy, no matter how small, and it derives not from the interface used or the time required, but from the very act of deciding.

Micropayments, like all payments, require a comparison: "Is this much of X worth that much of Y?" There is a minimum mental transaction cost created by this fact that cannot be optimized away, because the only transaction a user will be willing to approve with no thought will be one that costs them nothing, which is no transaction at all.- Clay Shirky8

In the world of financial payments, small fees are acceptable because the value of the transaction is extremely high relative to the fee charged, and the buyer has already made a decision to buy. The world of potential blockchain applications is far greater than just financial payments and includes many necessary transactions for which fees are simply unacceptable to users.

Systems like BitShares, Nxt, Ripple, Counter Party and Stellar all allow users to place limit orders on the blockchain and all of them charge users a small fee to perform this action. Later if the user wishes to cancel their order, another fee is charged. Systems like Ethereum take micropayments to a whole new level: charging per calculation. All of these systems struggle to attract new mainstream users for the same reasons that a decentralized search engine would struggle to attract users from Google if it charged a small fee for every search. It doesn't matter how good the service is, people expect certain things to be free. This is true even if a user ends up paying more overall under a different fee structure.

Fees are a Barrier to Entry

Any fee creates a barrier to entry for new users. Before someone can experiment with Ethereum they must acquire some ETH tokens. Anyone wanting to build a decentralized application on Ethereum must pass on the cost to their customers. Buying a crypto currency is not an easy task and rarely makes sense for amounts less than $10. This means that new users wanting to try out a new decentralized application must first be convinced to part with $10.

Changing Fees

Over time a network must adjust fees. This can happen either due to an increase in the value of the token or due to a surge in capacity. Users like predictable fees and guaranteed service. While it is possible to dynamically adjust fees during times of heavy use, the result is a poor user experience.

Sybil Attacks

Centralized websites prevent spam through rate limiting and some form of ID verification. Even something as simple as reCAPTCHA 9 is sufficient to limit the creation of fake accounts. If someone abuses their account then centralized websites are free to block the account.

In a decentralized system there is no direct way to ban users nor centralized provider able to host a reCAPTCHA and enforce rate limiting of accounts. In fact, the inability to censor users is one of the main selling points of blockchain technology.

Full Reserve vs Fractional Reserve

Let's view a blockchain like an Internet Service Provider (ISP) co-op which owns all of the cables in the town and has a maximum amount of bandwidth that it can provide at any time. People living in the town can buy shares in the ISP and in exchange they are entitled to utilize a portion of the available bandwidth.

The ISP has two choices, run a "full reserve" or "fractional reserve" system. Under a full reserve system each user is only allowed a fraction of the maximum bandwidth proportional to her shares. Because not everyone uses the Internet at the same time, the town's network would be significantly underutilized.

Under a fractional reserve system the individual users could utilize more bandwidth than they are entitled to at any given point in time so long as not everyone uses the Internet at the same time. The problem with operating a fractional reserve is that congestion occurs anytime too many people wish to use the network at the same time. The ISP needs a way to prioritize bandwidth during congested periods. In the most extreme case, a fully congested network must revert to a full reserve system. The challenge is setting the proper fractional reserve ratio.

Bandwidth Instead of Micropayment Channels

The solution to the problems with micropayments is in implementing dynamic fractional reserves. Under this model the blockchain will automatically adjust the reserve ratio for the network during times of congestion. The blockchain will set a target utilization that leaves enough headroom for short term surges in demand. Any time the surges are sustained the blockchain reduces the maximum bandwidth-per-share. When a surge is over and there is surplus capacity the blockchain can slowly increase the bandwidth-per-share.

Bandwidth used by an individual user should be measured over a suitably long period of time to allow that user to time-shift their usage. Users tend to login, do many things at once, then logout. This means that their bandwidth over a short period of time may appear much higher than if viewed over a longer period of time. If the time window is stretched too far then the reserve ratio will not adjust fast enough to respond to short-term surges, if the window is too short then clustering usage will have too big of an impact on normal users.

In our estimate it should be sufficient to measure the average weekly bandwidth usage of users. Every time a user signs a transaction, that transaction is factored into their own individual moving average. Any time a user's moving average exceeds the current network limit their transaction is delayed until their average falls below the limit.

Example Implementation

Let B equal a user's average bandwidth at time T. Let W equal the number of seconds per week, and let N equal the size of the new transaction that occurred S seconds after T. Given this information the blockchain can calculate the new average bandwidth for a user as:

Bnew = MIN(0,B * (W - S) / W) + N * S / W

Tnew = T + S

Each user is entitled to an average weekly bandwidth of:

Let U = the user's SP

Let S = the total number of SP

Let R = the current reserve ratio between 1 and Rmax

Let C = the maximum block size capacity set by witnesses

Let L = the total blocks per week

Let M = C * L * R

Allocation = M * U / S

A user would be entitled to an average bandwidth of M * U / S. Any time a transaction would cause the user's average to go above this threshold they would be unable to transact until enough time passes to lower the average.

The network can increase the reserve ratio, anytime blocks are less than half the target capacity and decrease it anytime they are more than half. The algorithm used to adjust R is designed to react quickly to decrease the reserve ratio when there is a surge in demand, while acting slowly to increase the reserve ratio in period of low demand.

The minimum reserve ratio is 1, and the maximum reserve ratio should be calculated to prevent small stakeholders from consuming all of the available bandwidth. If no one is using the available bandwidth then the reserve ratio can grow until a user with just 1 satoshi of the currency is able to transact every single block.

Case Study: Bitcoin

To understand how this algorithm would work on Bitcoin it is necessary to estimate a reasonable value for the reserve ratio, R, based on actual usage. Based upon the total supply of 15M BTC and a daily transaction volume of 400K BTC10, we can derive a minimum reserve ratio of 38 for Bitcoin. Using the equations we can calculate the weekly bandwidth (in bytes) allowed per BTC to be:

Let C = 1MB = 1024 * 1024

Let L = 1008 (blocks per week)

Let R = 38

Let S = 14000000 BTC (supply minus Satoshi's unmoving coins)

Let U = 1 BTC

CLR/S = 2869 bytes per week, or about 5 transactions/week per BTC

Since R = 38 is a lower bound on the reserve ratio, CLR/S is a lower bound on the permitted bandwidth. This simple case study suggests a user will require at most 0.20 BTC (over $80 as of this writing) to transact once per week. However, this is a loose upper bound derived from the assumption that all BTC are equally mobile. This is not the case - users with dozens or hundreds of bitcoins do not necessarily transact dozens or hundreds of times a week! The "leftover" transactions that those users "should" have made will increase the reserve ratio, allowing their unused bandwidth to be "recycled" for smaller users.

All of the above estimates are conservative upper bounds assuming coins and usage are distributed in a relatively flat manner. The reality is that heavy users, such as exchanges, have a much higher coin-to-usage ratio than lighter users, which in turn means that actual minimum balance requirements are far lower.

Impact of Capacity

Blockchain capacity isn't necessarily capped. It is well within the technological capability of internet infrastructure to increase the Bitcoin block size to 10MB which in turn will reduce the minimum required balance by a factor of 10. While Bitcoin currently supports about 3 transactions per second, alternative implementations are capable of over 1000 transactions per second. This changes our conservative upper bound to 0.0006 BTC or about $0.25, meaning that an account holding $0.25 would be able to transact at least once per week on average (and likely many more times because we're dealing with a fairly loose upper bound).

Maximum Number of Unique Users

We can use similar math to calculate the maximum number of unique users that the network can allow to transact once per week as: B*W/T. T represents the average transaction size. This means Bitcoin could support about 2 million users transacting once per week assuming each user had an equal balance.

Comparison to Fees

If we assume a user with $25 dollars worth of BTC transacts once per week and pays a $0.04 cent fee each time then they would pay over $2.00 in fees per year. A user would have to earn a 8% rate of return on their $25 dollars just to break even with paying fees. Chances are that users were going to hold their money on the blockchain anyway, so this user with $25 worth of BTC just saved $2 over the course of a year by adopting a rate-limiting approach rather than a fee-based approach. With just $175 they could transact every single day and save $14 per year.

Account Creation

Steem's account-based system with publicly known balances simplifies the implementation of the bandwidth-based rate limiting algorithm. Any account with a balance below the minimum required to transact once per week would be unable to transact. This implies that all new accounts should be funded with at least this minimum balance. It also implies that users wishing to transact in smaller amounts can, so long as they hold a larger balance and reuse the account.

It is possible for a low-balance account created during a time of low usage to become inaccessible if the network usage picks up. The funds could be recovered at any time by transferring a larger balance into the account.

In order to maintain a reasonable user experience with a minimum number of hung accounts, all new accounts should start out with a balance 10 times the minimum required to transact weekly. This way even if demand increases by a factor of 10 the account will remain viable.

Any initial account balance would have to come from the user creating the account and not from token creation due to the potential for sybil attacks.

Justifying Minimum Balances

The concept of forcing users to maintain a minimum balance flows naturally from the value of a user11 . Anyone running a business knows that every single user has significant value. Businesses spend anywhere from $30 to $200 to acquire a user. Sometimes they pay users directly, other times they pay for advertizing, and still other times entire companies are bought just for their user base. After a company acquires a user they often given them many free services just to keep them around long enough to monetize them through some other means.

Ripple uses a minimum balance12 that scales with account resource use and requires that new accounts get funded with at least this minimum balance. Currently this minimum balance is about $0.15 which is greater than the $0.10 we estimated would allow someone to transact freely at least once per week.

A blockchain can enforce a minimum value per user through the simple process of requiring a minimum balance. Any business that wishes to bring a new customer to the blockchain can pre-fund that user's account with the minimum balance that would allow them to transact. Requiring a relatively large fee ($1.00) to sign up new users will naturally force anyone offering free accounts to vet the quality and uniqueness of each account before registering them with the blockchain.

Maintaining a minimum balance is effectively the same as making users pay transaction fees with the interest they could have earned on their balance. The minimum balance is simply the balance required to earn enough interest to pay a fee in a relatively short period of time.

Fortunately, the minimum balance required can be as low as a dollar and this is something users can understand and appreciate. The opportunity cost of lost interest doesn't incur the cognitive cost of a micro-fee and is far more acceptable to users.

The STEEM used to pre-fund an account is Powered Up in the new account (i.e., converted to Steem Power).

Adjusting the Reserve Ratio

Rate limiting requires that the network adjust the reserve ratio quickly enough to mitigate the impact of an attacker attempting to ood the network. Let's assume the attacker has a large balance, say 1% of the available tokens. If we also assume that the network targets 50% utilization, then a sustained attack should find this user throttled to 25% of network capacity assuming everyone else is also using 25% of the capacity. Stated another way, the largest single user should never be able to consume more than 50% of the target capacity unless they own more than 50% of the SP.

Let's use an initial reserve ratio of 200x. Due to fractional reserves, this means someone holding 1% of the tokens has the right to demand transactions totalling 2x the maximum block size. In order to bring the network usage of the attacker down to 25% the reserve ratio would have to fall to 25x. This would cause the minimum balance required to transact once per week to grow by 8x.

The blockchain can establish a response rate that says any sustained increase in usage should be brought down to the target capacity in within a short period of time (say 30 seconds). An attacker attempting to spam the network shouldn't be able to disrupt service for normal users for more than a minute.

While reductions in the reserve ratio must be quick and non-linear to counter abuse, increases in the reserve ratio should be slow and linear. If the network adjusted in both directions in just 30 seconds then an attacker could pulse the network. A flood of transactions should be corrected in 30 seconds and then take a hour to return to their pre-attack levels. Under this model the attacker could flood the network for 30 seconds per hour or less than 1% of the time.

There must be a slow constant upward pressure on the reserve ratio any time network usage is below 50% until the network hits the maximum reserve ratio. The maximum reserve ratio determines the minimum required stake to flood the network in short bursts.

Any user with fewer than TOTAL_TOKENS / (2 * RESERVE_RATIO) will be unable to produce enough transactions to fill even a single block. With a reserve ratio of 200, this means any user with less than 0.25% of the currency cannot create enough transactions to delay anyone's service.

Effectiveness Relative to Fees

To compare the effectiveness of rate limiting to fees we must consider how the two systems react to intentional network flooding by an attacker. Under Bitcoin an attacker with $10,000 dollars could disrupt service for an entire day by filling every single block. The same attacker would be unable to disrupt service for even a single block under the dynamic fractional reserve rate limiting approach.

If we go to a more extreme case and assume the attacker holds 1% of all coins then we presume an attacker with $60 million dollars. Such an attacker could deny the Bitcoin blockchain service for 16 years unless the miners increased fees or capacity. Even if fees were raised to $15 per transaction, the attacker could still keep the network flooded for 16 days.

Under the rate limiting approach, someone who holds 1% of all coins with an intent to flood the network would achieve their goal for less than 30 seconds.

Renting vs. Buying vs. Time Sharing

When someone owns a house they expect the right to use the house for free. If a group of people buy a house together then each can expect the right to use the house proportional to their percentage ownership in the house. A fee based blockchain is like renting the house from its owners, whereas rate limiting is like a timeshare among owners.

If a house is owned by multiple people then those individuals must decide how they wish to timeshare the house. Someone who owns 50% of the house but only uses it one weekend per year might expect to be paid by the individuals who take their unused time. This is the mindset of a fee based system.

On the other hand, someone who owns 50% of the house is speculating that demand for the house will increase in the future and they will be able to sell their stake for more. Any owner who owns more of a house than they use becomes a real estate speculator. With this mindset rather than collecting rent, they collect appreciation.

The value of a share is derived from how much time it can potentially grant its owner. Owning 1% of a house and getting it 1 weekend per year is the lowest value of a share. However, if half of the shareholders never use their weekend, then the value per timeshare rises to 2 weekends per year. If those inactive users instead opt to rent their unused time, then it falls back to 1 weekend per year. If those unused timeshares were sold to people who would use them then the value of a timeshare would fall by 50%. Unless the rent collected is greater than the fall in share value the timeshare owners are making an economic miscalculation.

Using this rationale we can assume that a system based on fees will either be more expensive for its users or be less profitable for its collective owners. An individual small owner may profit by renting out his small time slice, but only at the expense of all other timeshare owners. In effect, the cost of the falling timeshare value is shared among all owners whereas the profits are centralized in the single owner who decided to rent his share.

We can conclude from this that a blockchain is best served by not using usage fees at all. If a usage fee were to be charged as an alternative to rate limiting, then it should be the equivalent of buying enough timeshares and committing to hold them long enough to gain the right use it once.

Stated another way, a transaction fee should be equal to the minimum account balance necessary to transact once per week and it should be refunded at the end of the week. Assume the minimum account balance is $1 and allows someone to transact once per week. If someone with a $1 balance that wishes to perform 5 transactions at once they will have to increase their balance to $5 for a week either before or after their transactions.

In theory a market could form where users can borrow the stake required. In practice it is more efficient for users to simply buy and sell the timeshares necessary to meet their desired usage rate. In other words, the cost of negotiating micro-loans is greater than the cost of maintaining a balance suitable for your maximum weekly usage.

Decentralized rate limiting of transactions can enable new types of decentralized applications that were not viable when every use of the application required a micropayment. This new model gives application developers the ability to decide if and when to charge their users for transactions.

Performance and Scalability

The Steem network is built upon Graphene, the same technology that powers BitShares. Graphene has been publicly demonstrated sustaining over 1000 transactions per second on a distributed test network. Graphene can easily scale to 10,000 or more transactions per second with relatively straightforward improvements to server capacity and communication protocols.

Reddit Scale

Steem is capable of handling a larger userbase than Reddit. In 2015 Reddit's 8.7 million users generated an average of 23 comments per second13 , with an average of 83 comments per year per user. There were 73 million top-level posts, for an average of 2 new posts per second. There were about 7 billion up votes creating an average voting rate of 220 votes per second. All told, if Reddit were operating on a blockchain it would require an average of 250 transactions per second.

To achieve this industry-leading performance, Steem has borrowed lessons learned from the LMAX Exchange14, which is able to process 6 million transactions per second. Among these lessons are the following key points:

- Keep everything in memory.

- Keep the core business logic in a single thread.

- Keep cryptographic operations (hashes and signatures) out of the core business logic.

- Divide validation into state-dependent and state-independent checks.

- Use an object oriented data model.

By following these simple rules, Steem is able to process 10,000 transactions per second without any significant effort devoted to optimization.

Keeping everything in memory is increasingly viable given the recent introduction of Optanetechnology from Intel 15. It should be possible for commodity hardware to handle all of the business logic associated with Steem in a single thread with all posts kept in memory for rapid indexing. Even Google keeps their index of the entire internet in RAM. The use of blockchain technology makes it trivial to replicate the database to many machines to prevent loss of data. As Optanetechnology takes over, RAM will become even faster while gaining persistence. In other words, Steem is designed for the architectures of the future and is designed to scale.

Allocation & Supply

The Steem network starts with a currency supply of 0 and allocates STEEM via proof of work at a rate of approximately 40 STEEM per minute to miners, with an additional 40 STEEM per minute being created to seed the content and curation reward pools (for a total of 80 STEEM per minute). Then the network starts rewarding users who convert to SP. At this point, STEEM grows at a rate of approximately 800 STEEM per minute due to the combined effects of the various Contribution Rewards summarized below:

Contribution Rewards:

- Curation rewards: 1 STEEM per block or 3.875% per year, whichever is greater

- Content Creation rewards: 1 STEEM per block or 3.875% per year, whichever is greater

- Block production rewards: 1 STEEM per block or 0.750% per year, whichever is greater

- POW inclusion rewards before block 864,000: 1 STEEM per block (awarded as 21 STEEM per round)

- POW inclusion rewards after block 864,000: 0.0476 STEEM per block (awarded as 1 STEEM per round) or 0.750% per year, whichever is greater.